Raising the retirement age to 70 could save Social Security for us all

Despite an expected backlash, vocal objections and possible threats, it’s time to raise America’s Social Security retirement age to 70 years with no early retirement option.

There are important reasons for America to raise Social Security’s retirement age to 70 and do away with early retirement with reduced benefits, which about half of the recipients are currently choosing before reaching full retirement age.

The first has to do with the fact that Social Security is projected to be insolvent by 2035. In its 2022 annual report, the Social Security Board of Trustees concluded that if no changes are made, the program will not be able to meet its financial responsibilities by 2035.

A second reason for raising the retirement age to 70 centers on the increasing life expectancies of Americans that have occurred over the recent past.

When Social Security was passed in 1935, average life expectancies at birth for males and females in the U.S. were approximately 60 and 64 years, respectively, and the age to receive full benefits was set at 65 years. Nearly nine decades later, life expectancies at birth for males and females have increased by approximately 14 years, i.e., to 73 and 79 years, respectively.

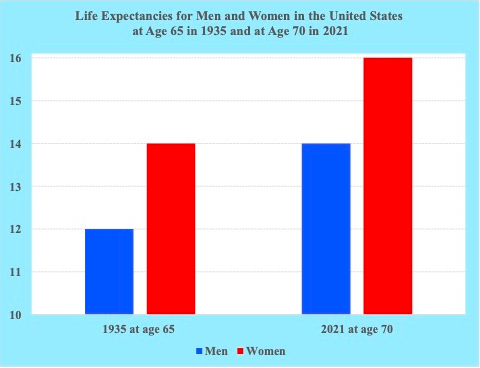

Moreover, U.S. life expectancies of men and women at older ages have increased significantly as well. In 1935, life expectancies at age 65 for men and women were approximately 12 and 14 years, respectively. In 2021 life expectancies for men and women at age 70 were approximately 14 and 16 years, respectively.

Source: Center for Disease Control (CDC).

In other words, due to the increases in life expectancies at older ages, raising Social Security’s retirement age for full benefits to 70 years would still provide men and women with more years in retirement than was envisaged when the program was established in 1935. On average, men and women in the U.S. reaching age 70 today can expect to live until ages 84 and 86, respectively, and those averages are expected to continue rising.

In addition to raising Social Security’s retirement age to 70, the early retirement option at age 62 with reduced benefits should be discontinued.

More than half of those applying for Social Security retirement choose to start their benefits before reaching their full retirement age. After deciding on early retirement, an individual’s Social Security benefits are provided at reduced levels for the remainder of the person’s life.

Many of those early retirees who elected to receive reduced benefits often find themselves in difficult financial circumstances later in life as they end up with insufficient funds. Raising the retirement age to 70 without the early retirement option would permit men and women more time to save for their retirement as well as provide them with full rather than reduced benefits in old age.

In addition, working longer offers health benefits. Remaining in the labor force encourages people to remain physically active and socially engaged.

Some have argued that raising Social Security’s retirement age would be unfair to some Americans because life expectancies vary with socioeconomic status. In brief, they stress that those at the lower end of the socioeconomic scale, such as janitors in Oklahoma, have significantly lower life expectancies at age 65 than those at the higher end, such as lawyers in New York. Those differences in life expectancy by socioeconomic status, however, were also the case when Social Security was first established.

Moreover, Social Security’s retirement age does not differentiate between men and women. Although women at age 65 years were expected on average to live several years longer than men, the ages to receive full benefits have continued to remain the same for both sexes.

Social Security’s retirement age also does not differentiate between major racial and ethnic groups. Despite the recognized sizable differences in the life expectancies between America’s major social groups, the age to receive Social Security benefits has been the same across the different groups.

Raising Social Security’s retirement age to 70 would provide an exemplary model for other countries. With the demographic aging of populations coupled with increasing longevity, countries worldwide are facing fewer people in the labor force per retired person and rising costs for the growing numbers of persons receiving retirement benefits.

A retirement age of 70 for both men and women would increase the size of the labor force, especially in those countries where the statutory retirement age is 65 years or less, such as France, Japan, Russia, and Sweden. Raising the retirement age to 70 also reduces the size of the retired population, the years in retirement and the cost of government retirement programs.

If Social Security’s retirement age is not raised, possible options to address the program’s expected insolvency include reducing benefits and increasing employment taxes. Those alternative options, however, are likely to be less acceptable than gradually raising the retirement age to 70.

While cutting benefits has been proposed by some congressional Republicans, such reductions would create financial problems for many retirees as well as be highly unpopular among the American public. Similarly, increasing employment taxes for Social Security is not likely to be well received by the business community, workers and congressional Republicans.

It should also be noted that the Social Security retirement age has been raised gradually over the recent past. For those born in 1960 or later, for example, Social Security’s retirement age to receive full benefits is now 67 years.

In coming years, lawmakers should remember that an increase in the retirement age to 70 with no early retirement option would address Social Security’s expected insolvency, compensate for increased longevity and expand the size of the labor force. It would also provide more time to save for retirement, preserve intergenerational equity and provide larger monthly benefits to retirees in old age.

Joseph Chamie is a consulting demographer, a former director of the United Nations Population Division and author of numerous publications on population issues, including his recent book, “Births, Deaths, Migrations and Other Important Population Matters.”

Copyright 2024 Nexstar Media Inc. All rights reserved. This material may not be published, broadcast, rewritten, or redistributed..