The Tax Cut and Jobs Act was a protein boost, not a sugar high

Recent release of full year 2018 Gross Domestic Product figures illustrates how the Tax Cut and Jobs Act (TCJA) that passed Congress in December 2017 boosted U.S. investment, growth and incomes.

TCJA cut both personal and corporate income taxes. Personal federal taxes in 2018 were 7.9 percent of GDP, down from 8.3 percent of GDP in both 2017 and 2016, the last year of President Barack Obama’s administration.

{mosads}The most significant TCJA effect was on federal corporate taxes, for which full-year data are not yet available. In 2018’s first three quarters, federal corporate taxes fell by 0.7 percent of GDP, a nearly 50-percent reduction from the comparable 2017 level of 1.5 percent of GDP. Overall, the 2018 federal tax take appears lower in 2018 than 2017 by 1.1 percent of GDP.

Far from producing a “sugar high,” as sometimes charged, TCJA was a protein booster. Tax savings were channeled primarily into savings and investment rather than consumption.

Personal consumption expenditures were lower in 2018 than 2017 by 0.3 percent of GDP, while investment increased by 0.5 percent of GDP to its highest level since before the financial crisis.

The investment boom is especially evident in numbers for the fourth quarter; private long-term investment, excluding residences, reached a level surpassed by just one previous quarter since 2001.

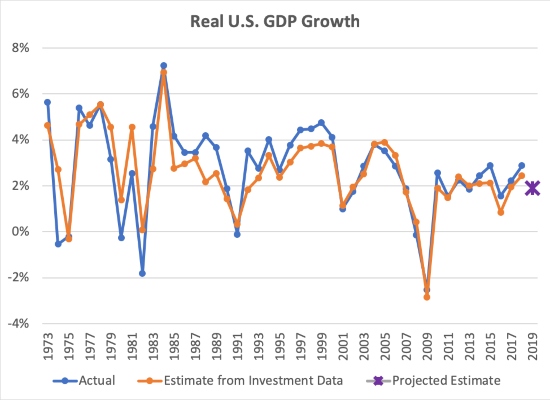

The strong investment response to the TCJA should alleviate concern about increased share repurchases and dividends. According to investment research firm Birinyi Associates, share repurchases grew more than $200 billion in 2018, 1.1 percent of GDP.

The economy’s investment boost demonstrates U.S. capital markets are doing what they should be doing: allocating resources from firms that lack investment opportunities to firms that have them.

An even greater hot button issue is wage growth. Economists across the political spectrum agree that investment is critical to improving the productivity and income of workers.

Workers’ income, measured by the Employment Cost Index that includes benefits, is strongly correlated with the level of investment. In 2018, compensation rose 3.1 percent, the fastest rate since the financial crisis.

The investment boost benefits economic growth in two ways. First, increased investment itself contributes to growth. Changes in the ratio of investment to GDP are reflected directly in the growth rate; a 1 percent increase in the investment ratio tends to result in a 1 percent increase in growth. This relationship explains over two-thirds of growth rate variability from 1980 to 2018.

Second, investment is productive, sparking yet more growth. From 1980 through 2014, the overall investment capital stock generated a 33.7 percent return in GDP output, according to data from the Penn World Table.

2018’s investment increase of 0.5 percent of GDP likely resulted in another 0.2 percent of growth, so new investment contributed a combined 0.7 percent to 2018 GDP growth.

Real GDP growth can be estimated from data on investment which includes: 1. change in the investment ratio and 2. the amount of investment less depreciation multiplied by the ratio of GDP to all investment capital stock.

Strong 2018 growth may be a difficult act to follow. If investment continues in 2019 at its 2018 level, the 0.2 benefit from capital productivity continues, but the 2018 boost of 0.5 percent from higher investment is no longer a factor, creating a significant headwind against 2018’s 3.1 percent growth.

As with building muscle from protein, ongoing work is needed just to stay at the same level. Further corporate tax cuts would strengthen and lengthen 2018’s investment and growth spurt.

Another downside is the federal deficit increase from TCJA. 2018 federal expenditures were even with 2017 relative to GDP, but the hole in taxes wasn’t filled, and the deficit increased by 0.8 percent of GDP.

Higher private savings financed the increased federal borrowing, but continued federal deficits can worsen the trade deficit. Any restraint of federal spending would improve the trade picture.

TCJA accomplished its proponents’ objective of investment-led economic growth, but standing in place means slipping back. More should be done for the American economy and people.

Douglas Carr is an associate fellow at R Street and is the president of Carr Capital Co., a financial and economic advisory firm.

Copyright 2024 Nexstar Media Inc. All rights reserved. This material may not be published, broadcast, rewritten, or redistributed..