Business investment has not soared

A recent headline from the Wall Street Journal boldly proclaimed, “Capital Investment Soars at Firms.” While making for a great headline, this is contrary to what first-quarter GDP numbers showed.

Intrigued, I read the article only to find out that capital investment had not soared, rather, Credit Suisse was estimating that it would soar. Reading on, I found the equivalent of “fine print” in the article, which stated the it was “expected” that capital expenditures at S&P 500 companies would increase in the first quarter.

That is very different than the pro-tax reform headline, which stated, “investment soars.” Second, the estimate is limited to S&P 500 companies. Flush with cash, it was never the largest companies that were starved for the money necessary to make investments, it was small businesses.

Of course S&P 500 investment will increase, the economy is expanding, and they have more cash than they know what to do with even after massive share buybacks.

Third, what will be the ratio of increases in investment to increases in share buybacks? Based on the pace of share buybacks, it is likely that increases in business investment will be far less than increases in share buybacks.

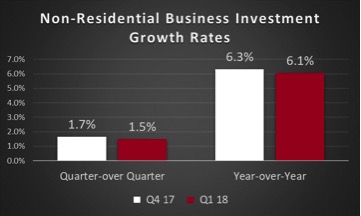

Looking at the facts and not expectations, the rate of growth in non-residential business investment declined in the first quarter on a quarter-over-quarter and year-over-year basis.

Whereas fourth-quarter non-residential business investment increased 1.7 percent on a quarter-over-quarter basis, Q1’s growth rate declined to 1.5 percent. Similarly, whereas Q4 non-residential business investment increased 6.3 percent on a year-over-year basis, Q1’s growth rate declined to 6.1 percent.

Source: Solutionomics using Bureau of Economic Analysis data

Looking at the facts and not headlines, the rate of growth in non-residential business investment declined across all companies after passage of the tax bill.

While business investment among S&P 500 companies may increase in the first quarter, it currently remains only an expectation, not reality, and it only reflects S&P 500 companies as opposed to the companies the economy really needs to increase investment — small businesses.

Given that that tax bill now provides for 100-percent and immediate deductibility of capital investments, why did the rate of growth in non-residential business investment decline as opposed to increase? Simple, demand is the primary drive of business investment, not tax rates.

Think about it. If you owned a business and your tax rate was cut but demand for your products remained the same, would you increase investment? Of course not.

That would be the equivalent of a CEO doubling his company’s production capacity when sales orders were little changed and when asked by the board of directors why production capacity was doubled saying, “because the tax rate was reduced.”

While tax rates can influence where investments in production occur, it is secondary to demand when determining whether to increase investment. Clearly, businesses so far have not seen the demand necessary to increase the business investment growth rate.

Even if the pace of business investment does increase, it may not be all it is cracked up to be. Why? There are no requirements for the equipment companies purchase to be made in America to be fully and immediately deductible.

This means a company can buy equipment produced outside of the U.S. generating jobs outside of the U.S. and receive full credit for buying the foreign-made equipment, and this is a very real possibility in today’s world.

As noted previously in another Solutionomics op-ed appearing in The Hill, more than 50 percent of global industrial robotics exports are from Japan and Germany.

It is very possible that the equipment businesses are receiving full and immediate tax deductibility on are made somewhere outside of the U.S. and generating jobs outside the U.S.

Flaws in the recently passed tax bill are bad enough. Confusing headlines relating to the effects of the changes in tax policy make the matter worse by reducing the understanding of the actual effects and the need to make the changes necessary to produce a more effective tax bill.

Chris Macke is the founder of Solutionomics, an economic think tank. He has advised the U.S. Federal Reserve by providing market updates and implications of monetary policy changes on asset valuations and market distortions, and he’s a contributor to the Fed Beige Book. Find him on Twitter: @solutionomics.

Copyright 2024 Nexstar Media Inc. All rights reserved. This material may not be published, broadcast, rewritten, or redistributed..

tt

Harris calls for ending filibuster for abortion rights