To avoid economic meltdown, the Fed should follow India’s COVID model

A looming banking crisis on the one hand and stubborn inflation on the other. That’s Federal Reserve Chairman Jerome Powell’s unenviable predicament. Powell would do well to recognize how the Fed’s monetary policy is leading to a banking crisis and pursue a course correction. Or else, the U.S. economy is looking at a prolonged winter.

Fortunately, there is a road map for navigating out of this crisis before it becomes an economy-wide meltdown — the way India handled the economic impact of the COVID-19 pandemic.

First, it’s important to understand why the Silicon Valley Bank fiasco is the canary in the coal mine. The Fed’s most aggressive rate hiking in four decades — from 0 percent to about 5 percent in just six months — precipitated this crisis.

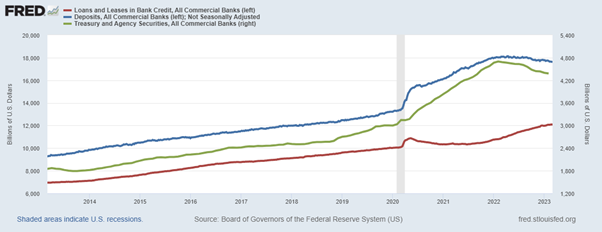

Post-pandemic, deposits at U.S. commercial banks increased from about $13 trillion to $18 trillion, as the chart below shows. However, this increase in deposits of $5 trillion was accompanied by an increase in lending by only $2 trillion. Banks were awash in cash and invested in securities.

Crucially, investment in Treasury and agency securities increased by $1.3 trillion; about half of this amount has a maturity of greater than 10 years. Longer-term securities are much more sensitive to interest rate changes. As a result, the Fed’s rapid increase in the interest rate led to heavy losses on the market value of these securities.

As estimates made by the FDIC highlight, unrealized losses on securities exceeded $600 billion. In December, the total equity of U.S. commercial banks was $2.2 trillion. This $600 billion loss translated into 30 percent of banks’ equity. This will inevitably translate into several banks’ becoming insolvent as their equity gets wiped out. Given this, the possibility of a widespread banking crisis is real.

The Fed must realize that further monetary tightening will only exacerbate the banking crisis. As a credit crisis has a long-term and pernicious effect on economic growth, raising rates additionally presents a very dangerous option.

Though confronted by stubborn inflation — core inflation continues to be sticky as the March data showed — U.S. policymakers must swallow the bitter pill that monetary tightening must end immediately. Otherwise, the spillovers from the banking crisis can lead to corporate defaults and another round of bank failures, arrest the flow of credit and stymie growth for several quarters.

With the option of monetary tightening removed from the table, U.S. policymakers would benefit from studying and learning from India’s economic policy response during COVID. Having helped design the policy that helped India successfully navigate the crisis, I can outline some lessons that will be valuable to U.S. policy today.

India entered the COVID pandemic in a bad place. Rating agencies had downgraded our country’s credit outlook. India’s sovereign rating was just one notch above non-investment grade. If Delhi had decided to counteract the economic harm of COVID by simply throwing money around, it could have led to a downgrade to non-investment grade, thereby triggering capital flight. At the same time, India had to cushion the economic impact on the poor and vulnerable.

We knew from experience during the Great Recession that excessive reliance on demand-side policies was not the answer, either. This led to double-digit inflation every month for 18 months, with India becoming part of the Fragile-5 economies. As India recognized early that the crisis would affect supply materially so it implemented supply-side measures. Delhi oriented its fiscal policy towards building infrastructure, undertook reforms to alleviate structural problems faced by firms, and provided incentives to firms to ramp up production in critical sectors.

As a result, at 6.4 percent in February this year, inflation in India is below the historical average of 7.5 percent and is within the country’s inflation target. Also, India expects to grow at a rate of 7 percent this decade. This robust economic performance has stemmed from a smart balance of demand and supply-side measures during the COVID crisis.

As Fed Chairman Powell and other U.S. policymakers struggle with the response to the current banking crisis, they realize there’s no silver bullet for the U.S. economy. It will take a smart balance of policies and patience to make certain the current banking crisis doesn’t spread to the entire system and the economy at large. The good news is, India’s successful navigation of its own recent crisis provides a way forward.

Krishnamurthy Subramanian is the executive director (India) of the International Monetary Fund and served as India’s chief economic advisor from 2018 to 2021.

Copyright 2024 Nexstar Media Inc. All rights reserved. This material may not be published, broadcast, rewritten, or redistributed..